How to Remain Compliant with ASC 842

To remain compliant with ASC 842, companies need to implement a structured approach that involves identifying and assessing all lease agreements both as lessees and lessors to accurately record lease liabilities and corresponding right-of-use assets. This entails capturing lease terms, determining appropriate discount rates, and regularly reassessing variables for changes. Robust internal controls and data management systems are essential to ensure accurate data collection and financial reporting.

In addition, companies must enhance their financial statement disclosures to provide comprehensive information about lease obligations, facilitating transparency and compliance with the standard's disclosure requirements. Regular training for personnel involved in lease management and accounting, as well as staying informed about updates or amendments to the standard, is crucial for ongoing adherence to ASC 842.

Free ASC 842 Compliance Checklist

Download the ASC 842 Compliance Checklist to simplify lease accounting, reduce audit risk, and stay on track with evolving standards.

How to Find the Best ASC 842 Lease Accounting Software

Finding the best ASC 842 lease accounting software involves a comprehensive evaluation of features, scalability, user-friendliness, integration capabilities with existing systems, compliance with the ASC 842 standard, and customer support. Prioritize solutions that offer robust lease data management, tracking of lease terms and changes, accurate financial reporting, and effective disclosure management. Consider user reviews and industry reputation to gauge reliability and performance.

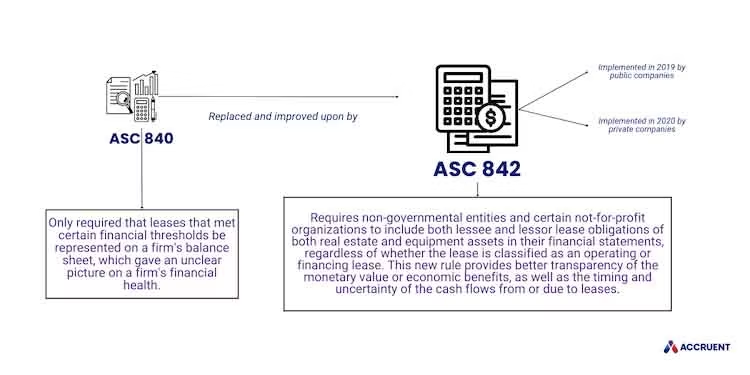

How ASC 842 Came to Be

ASC 842 came into existence as a result of the Enron fallout. At its height, Enron was a much riskier company than its published financial statements indicated in 2001. This was mostly due to its significant use of leases, which under the old leasing disclosure regulations -- FAS 13 / ASC 840 -- only required capital leases on the balance sheet.

Infamously, Enron fell on hard times, entering Chapter 11 bankruptcy in 2001, exiting said bankruptcy in 2004, all before selling its last asset in 2006. Along the way, shareholders lost over $11 billion, and the Sarbanes-Oxley Act of 2002 came into existence in an attempt to improve public firm disclosures and hold executives accountable. Enron's accounting firm Arthur Anderson was dissolved, and the SEC tasked the FASB to improve lease disclosures overall.

Requirements of ASC 842 Lease Accounting

ASC 842 requires companies to classify all leases as either finance or operating leases. According to Investopedia, a finance lease is like a rental contract where a lessee can use an asset, such as a car or other equipment, and, after the lease is over, they have the option to own it. However, the owner (lessor) must fulfill all of their responsibilities as outlined in the contract. An operating lease, on the other hand, allows the use of an asset without a transfer of ownership.

This classification determines how the lease is recognized on the balance sheet and income statement. For finance leases, companies must recognize an asset and liability equal to the present value of the lease payments. For operating leases, companies must recognize a lease liability and a corresponding right-of-use asset on the balance sheet.

Implications of ASC 842 Lease Accounting

The implementation of ASC 842 has significant implications for companies' financial statements. By recognizing all leases on the balance sheet, companies' total assets and liabilities will increase, which may impact their debt-to-equity ratios and other financial ratios. Companies will also need to provide additional disclosures about their leases, including lease term, discount rate, and lease payments.

Practical Considerations for Companies

The implementation of ASC 842 requires companies to gather detailed information about their leases, including lease terms, renewal options, and lease payments. This information may not be readily available, and companies may need to invest in new systems and processes to capture and report this data. Companies will also need to train their employees on the new standard and work closely with their auditors to ensure compliance.

ASC 842 Implementation Dates & Deadlines

For US public and all international companies, the deadline to comply with ASC 842 and IFRS 16 began for fiscal years beginning after December 15, 2018 for US public companies and January 1, 2019 for all international companies.

US private companies had until December 15, 2019 to comply with ASC 842, but received a reprieve in July of 2019 allowing a year-long extension and a new adoption date for fiscal years beginning after December 15, 2020.

What Does ASC 842 Mean for You?

ASC 842 requires organizations with lease assets to recognize nearly all leases as assets and liabilities, whether classified as operating leases or financing leases, subject to certain exemptions. For the lessee or lessor, the recognition of more ASC 842 governed lease-related assets and liabilities, as well as changes to the timing of lease expense recognition, has had significant financial reporting and business implications.

With the new ASC 842 and IFRS 16 accounting standards, compliance is more complicated and demands a higher level of internal effort. Whether it is finding leases, creating new workflows to manage them or understanding the new monthly closing process around them, ASC 842 and IFRS 16 require more work.

Fortunately, ASC 842 software can help.